Introduction

In the world of small and medium-sized enterprises (SMEs), cash flow management is often a top concern. Maintaining a healthy cash flow is vital for the sustainability and growth of your business. One powerful tool that SME business owners can use to assess and improve their cash flow is the Cash Conversion Cycle (CCC).

In this post, I want to delve into the practical use of the CCC for SME business owners, exploring what it is, why it matters, and how you can optimize it to keep your business thriving.

Chapter 1: Understanding the Cash Conversion Cycle (CCC)

1.1. Days Inventory Outstanding (DIO)

Definition and Importance of DIO:

The Days Inventory Outstanding (DIO) is a critical component of the Cash Conversion Cycle (CCC). It represents the average number of days it takes for a business to sell its inventory. Understanding and managing the DIO is essential because it directly affects your business’s cash flow and overall financial health.

A shorter DIO is generally more favorable for SMEs, as it signifies that your inventory is moving quickly, reducing the amount of capital tied up in unsold goods. This, in turn, allows for more agile cash flow management and greater liquidity.

Calculating DIO:

To calculate the DIO, use the following formula:

DIO = (Average Inventory / Cost of Goods Sold) x Number of Days in the Period

Average Inventory is the average value of your inventory over a specific period.

Cost of Goods Sold (COGS) is the cost incurred to produce or purchase the inventory items.

Number of Days in the Period refers to the length of the period under consideration.

Factors Affecting DIO:

Several factors influence the DIO:

Demand Variability: Fluctuations in customer demand can impact how quickly inventory is sold.

Production Lead Times: Longer lead times can extend the DIO.

Inventory Management Practices: Effective inventory management strategies can help reduce DIO by minimizing excess stock and optimizing reordering.

1.2. Days Sales Outstanding (DSO)

Definition and Importance of DSO:

The Days Sales Outstanding (DSO) is the average number of days it takes for a business to collect payments from customers after making a sale on credit.

A shorter DSO is advantageous as it indicates that customers are paying promptly, ensuring a steady inflow of cash.

Effective management of DSO is crucial because it directly impacts your business’s cash flow and liquidity. A longer DSO can strain your finances, especially if your business relies heavily on credit sales.

Calculating DSO:

To calculate the DSO, use the following formula:

DSO = (Average Accounts Receivable / Total Credit Sales) x Number of Days in the Period

Average Accounts Receivable represents the average amount of money owed to your business by customers.

Total Credit Sales is the total value of sales made on credit during the specific period.

Number of Days in the Period is the length of the period being analyzed.

Strategies to Reduce DSO:

To shorten the DSO and improve cash flow, consider implementing these strategies:

Effective Credit Policies: Establish clear credit policies, credit limits, and payment terms for customers.

Incentives for Early Payments: Offer discounts or other incentives to encourage customers to pay their invoices promptly.

Streamlining Invoicing and Collections: Optimize your invoicing and collections processes to minimize delays in payment.

1.3. Days Payable Outstanding (DPO)

Definition and importance of DPO:

Days Payable Outstanding measures how long it takes for a business to pay its suppliers after receiving goods or services. A longer DPO allows your business to hold onto cash for a longer period, but it should be balanced to maintain good relationships with suppliers.

Managing the DPO strategically is essential for cash flow optimization, as it affects your ability to meet financial obligations while preserving working capital.

Calculating DPO:

To calculate the DPO, use the following formula:

DPO = (Average Accounts Payable / Cost of Goods Sold) x Number of Days in the Period

Average Accounts Payable is the average amount your business owes to suppliers.

Cost of Goods Sold (COGS) is the cost of goods or services purchased during the period.

Number of Days in the Period is the length of the period under analysis.

Strategies to Optimize DPO:

To extend the DPO and retain cash for longer, consider these strategies:

Negotiating Favorable Payment Terms with Suppliers: Discuss payment terms with suppliers to find mutually beneficial arrangements, such as extended payment periods.

Cash Flow Forecasting for Payment Scheduling: Use cash flow forecasting to plan supplier payments strategically and avoid late fees.

Vendor Relationships and Communication: Building strong relationships with suppliers and maintaining open communication can lead to more flexible payment terms.

Chapter 2: Why the CCC Matters for SMEs

Understanding the significance of the CCC for SMEs is crucial for effective cash flow management and overall business success.

2.1. Cash Flow Management

How the CCC Impacts Your Business’s Cash Flow:

The CCC has a direct and substantial impact on your business’s cash flow. A shorter CCC means quicker access to cash, while a longer CCC can tie up capital and hinder your ability to meet financial obligations.

Imagine your business has a CCC of 90 days. This means it takes 90 days, on average, to convert your investments in inventory and accounts receivable into cash. During this time, you need sufficient liquidity to cover operating expenses, pay suppliers, and invest in growth opportunities. A prolonged CCC can strain your cash flow and put your business at risk.

The Link Between CCC and Liquidity:

Liquidity refers to your business’s ability to meet its short-term financial obligations. A well-managed CCC contributes to improved liquidity, ensuring you have sufficient cash on hand to cover expenses and investments.

When your CCC is optimized, you can better navigate unexpected expenses or take advantage of opportunities like bulk purchasing to secure discounts. In contrast, a lengthy CCC may require external financing to bridge gaps in liquidity, leading to interest expenses and potential financial stress.

2.2. Working Capital Efficiency

The Relationship Between CCC and Working Capital:

Working capital is the capital used for day-to-day operational expenses, including purchasing inventory, paying employees, and covering overhead costs. An optimized CCC ensures that working capital is utilized efficiently, preventing excessive capital from being tied up in inventory and accounts receivable.

Inefficient working capital management can result in underutilized resources and missed growth opportunities. For SMEs, which often operate with limited resources, optimizing working capital through CCC management can make a significant difference in sustaining and expanding the business.

The Role of Working Capital in Daily Operations:

Working capital is the lifeblood of your business’s daily operations. It ensures you have the funds necessary to pay suppliers, meet payroll, and seize opportunities for growth. Without adequate working capital, your business may struggle to cover its obligations, leading to financial distress.

By aligning your CCC with your working capital needs, you can strike a balance between maintaining a healthy cash reserve and investing in your business’s growth and competitiveness.

2.3. Profitability

How Optimizing the CCC Can Boost Your Profitability:

Profitability is a key metric for measuring your business’s success. An optimized CCC plays a vital role in enhancing profitability. Here’s how:

Reduced Financing Costs: A shorter CCC reduces the need for external financing, such as loans or lines of credit, to cover operational gaps. This, in turn, reduces interest expenses and improves your bottom line.

Faster Reinvestment: A shorter CCC allows you to reinvest cash into profitable activities more quickly. Whether it’s expanding your product line, launching marketing campaigns, or investing in research and development, having ready access to cash can accelerate growth.

Improved Supplier Negotiations: With the ability to pay suppliers on time or negotiate favorable terms due to an extended DPO, you can secure discounts, reduce procurement costs, and enhance overall profitability.

Examples of how Businesses Benefiting from CCC Improvements:

To illustrate the impact of CCC optimization, let’s explore a couple of real-life examples:

Example 1: Retail Store

A small retail store successfully reduced its DIO by implementing efficient inventory management practices. By regularly assessing demand patterns and using technology to automate reordering, they reduced excess stock and improved cash flow. This allowed them to allocate more resources to marketing and expanding their product range, ultimately increasing sales and profitability.

Example 2: Manufacturing Company

A manufacturing company streamlined its production processes and improved its DSO through effective credit policies. By offering discounts for early payments and closely monitoring outstanding invoices, they incentivized customers to pay promptly. This ensured a steady inflow of cash, allowing the company to invest in equipment upgrades and enhance production efficiency, further boosting profitability.

These examples demonstrate that optimizing the CCC is not merely a financial exercise but a strategy that can directly impact your SME’s profitability and long-term viability.

Chapter 3: Calculating Your CCC

To effectively manage your CCC, it’s essential to know how to calculate it accurately. In this chapter, we’ll provide step-by-step instructions on calculating your CCC and offer practical examples and templates for your reference:

3.1. Formula for CCC Calculation

Understanding the CCC Formula:

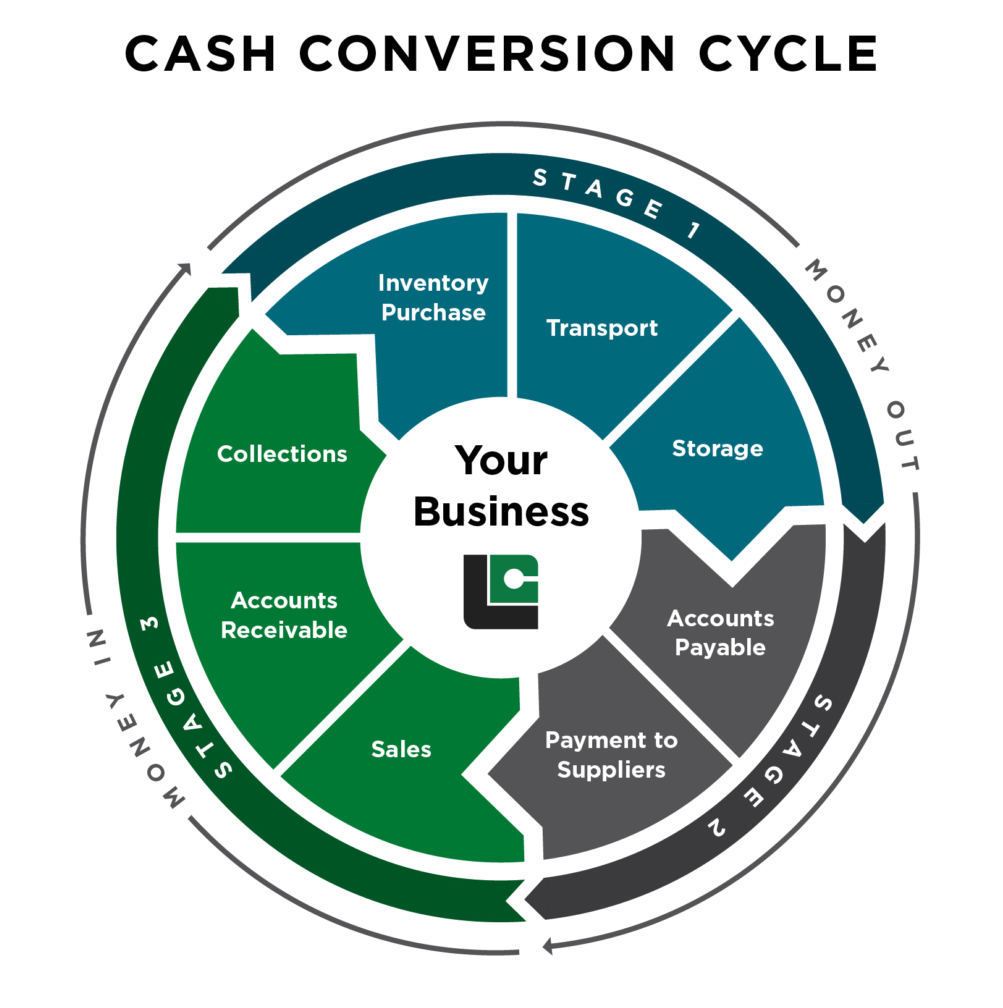

The Cash Conversion Cycle (CCC) formula is a powerful tool for assessing the efficiency of your business’s working capital management. It combines three key components—Inventory Conversion Period (DIO), Receivables Conversion Period (DSO), and Payables Conversion Period (DPO)—to provide a comprehensive view of how effectively your business converts investments into cash.

The formula is as follows:

CCC = DIO + DSO – DPO

Understanding each component’s role and how they interact is crucial to interpreting your CCC correctly.

How Each Component Contributes to the Overall CCC:

DIO measures how long it takes to sell inventory and represents the capital tied up in unsold goods.

DSO assesses how quickly you collect receivables and determines the cash tied up in accounts receivable.

DPO evaluates how long it takes to pay suppliers and indicates the potential to hold onto cash for a longer period.

By optimizing each of these components, you can positively influence your CCC and improve your business’s cash flow.

3.2. Real-Life Examples

Walkthroughs of CCC Calculations for Different Types of SMEs:

Let’s consider two hypothetical SMEs to illustrate how CCC calculations work:

Example 1: Online Retailer

Days Inventory Outstanding (DIO): The online retailer, XYZ Electronics, sells consumer electronics. They had an average inventory value of $200,000 during the year, with COGS amounting to $800,000.

Calculating DIO:

DIO = ($200,000 / $800,000) x 365 = 91.25 days

XYZ Electronics takes an average of 91.25 days to sell its inventory.

Days Sales Outstanding (DSO): XYZ Electronics offers credit terms to customers, resulting in an average accounts receivable of $50,000. Their total credit sales for the year were $600,000.

Calculating DSO:

DSO = ($50,000 / $600,000) x 365 = 30.42 days

It takes XYZ Electronics an average of 30.42 days to collect payments from customers.

Days Payable Outstanding (DPO): XYZ Electronics negotiates favorable terms with suppliers, resulting in an average accounts payable of $40,000. Their COGS for the year was $800,000.

Calculating DPO:

DPO = ($40,000 / $800,000) x 365 = 18.25 days

XYZ Electronics takes an average of 18.25 days to pay suppliers.

Now, using the CCC formula:

CCC = DIO + DSO – DPO

CCC = 91.25 + 30.42 – 18.25 = 103.42 days

XYZ Electronics has a CCC of approximately 103.42 days.

Example 2: Manufacturing Company

Days Inventory Outstanding (DIO): ABC Manufacturing produces custom machinery. They had an average inventory value of $500,000 during the year, with COGS amounting to $2,000,000.

Calculating DIO:

DIO = ($500,000 / $2,000,000) x 365 = 91.25 days

ABC Manufacturing takes an average of 91.25 days to sell its inventory.

Days Sales Outstanding (DSO): ABC Manufacturing extends credit terms to clients, resulting in an average accounts receivable of $100,000. Their total credit sales for the year were $1,200,000.

Calculating DSO:

DSO = ($100,000 / $1,200,000) x 365 = 30.42 days

It takes ABC Manufacturing an average of 30.42 days to collect payments from clients.

Days Payable Outstanding (DPO): ABC Manufacturing negotiates payment terms with suppliers, resulting in an average accounts payable of $80,000. Their COGS for the year was $2,000,000.

Calculating DPO:

DPO = ($80,000 / $2,000,000) x 365 = 14.6 days

ABC Manufacturing takes an average of 14.6 days to pay suppliers.

Using the CCC formula:

CCC = DIO + DSO – DPO

CCC = 91.25 + 30.42 – 14.6 = 107.07 days

ABC Manufacturing has a CCC of approximately 107.07 days.

These examples illustrate how CCC calculations work for different types of businesses and show that optimizing your CCC can lead to improved cash flow management.

Analyzing the Results:

In both examples, businesses can use their CCC values to assess the efficiency of their working capital management.

A lower CCC indicates a quicker conversion of investments into cash, which is generally favorable for cash flow. Analyzing the CCC can help identify areas for improvement and guide financial strategies.

Chapter 4: Strategies to Optimize Your CCC

Now that you understand the CCC and how to calculate it, let’s explore strategies to improve each component:

4.1. Reducing Days Inventory Outstanding (DIO)

Inventory Management Techniques:

Effective inventory management is crucial for reducing DIO. Consider implementing the following techniques:

ABC Analysis: Categorize your inventory into A, B, and C items based on their importance. Focus on optimizing the management of high-value A items.

Safety Stock: Maintain a safety stock level to account for unexpected demand fluctuations or supplier delays.

Economic Order Quantity (EOQ): Calculate the optimal order quantity to minimize carrying costs and ordering costs.

Lean Inventory Principles: Adopt lean principles to minimize waste and reduce excess inventory:

Just-in-Time (JIT): Implement a JIT inventory system to receive goods only when they are needed, reducing excess stock and storage costs.

Kanban System: Use a kanban system to signal when to reorder inventory items, optimizing replenishment.

Supplier Collaboration: Collaborate closely with suppliers to improve demand forecasting and streamline supply chains.

4.2. Shortening Receivables Conversion Period (DSO)

Effective Credit Policies:

Establish clear credit policies to encourage timely customer payments:

Credit Limits: Set appropriate credit limits based on customer creditworthiness to minimize the risk of late payments or defaults.

Payment Terms: Define clear payment terms, such as net 30 or net 60, to specify when payments are due.

Credit Monitoring: Regularly review customer credit accounts and adjust credit terms as needed.

Incentives for Early Payments: Offer incentives to encourage customers to pay their invoices promptly:

Early Payment Discounts: Provide discounts for early payments, such as a 2% discount for payment within 10 days.

Customer Loyalty Programs: Reward repeat customers with special offers or discounts for on-time payments.

Late Payment Penalties: Consider imposing penalties for late payments to motivate timely settlements.

Streamlining Invoicing and Collections:

Optimize your invoicing and collections processes to minimize delays in payment:

Automation: Use accounting software to automate invoicing and reminders for overdue payments.

Clear Invoices: Ensure that invoices are clear, accurate, and include all necessary details, reducing disputes and delays.

Effective Collections: Implement a systematic approach to collections, escalating efforts for overdue accounts.

4.3. Extending Days Payable Outstanding (DPO)

Negotiating Favorable Payment Terms with Suppliers:

Effective negotiation with suppliers can extend the DPO:

Extended Payment Terms: Negotiate for longer payment terms, such as net 60 or net 90, to hold onto cash for an extended period.

Bulk Discounts: Explore opportunities for bulk purchasing or volume discounts to reduce procurement costs.

Supplier Financing: Inquire about supplier financing options that allow for delayed payments without incurring interest or penalties.

Cash Flow Forecasting for Payment Scheduling:

Implement cash flow forecasting to plan supplier payments strategically:

Cash Flow Analysis: Analyze your cash flow patterns to determine the best timing for supplier payments.

Prioritization: Prioritize payments based on supplier terms, avoiding late fees or penalties.

Working Capital Loans: Consider short-term working capital loans to bridge gaps between accounts payable and accounts receivable.

Vendor Relationships and Communication:

Building strong relationships with suppliers and maintaining open communication can lead to more flexible payment terms:

Regular Communication: Keep suppliers informed of your payment plans and any potential delays.

Early Payment Negotiation: If your cash flow allows, offer early payments in exchange for discounts.

Long-Term Partnerships: Cultivate long-term relationships with key suppliers to strengthen negotiating positions.

Implementing these strategies can help optimize your CCC and enhance your business’s cash flow, allowing for more efficient working capital management.

Chapter 5: Monitoring and Continuous Improvement

Improving your CCC is an ongoing process. In this chapter, we’ll discuss how to monitor your progress and continuously enhance your CCC:

5.1. Key Performance Indicators (KPIs)

Metrics to Track the Effectiveness of Your CCC Improvements:

To gauge the success of your CCC optimization efforts, monitor key performance indicators (KPIs) regularly:

CCC Value: Keep an eye on your CCC value, tracking it over time to ensure it’s trending in the desired direction.

DIO, DSO, and DPO: Monitor each component individually to identify areas requiring further improvement.

Working Capital Ratio: Assess your working capital ratio to ensure it remains at healthy levels.

Cash Flow Forecast Accuracy: Measure the accuracy of your cash flow forecasts against actual results to fine-tune your predictions.

Setting Benchmarks and Targets: Set benchmarks and targets for your CCC and related KPIs:

Industry Benchmarks: Compare your CCC against industry benchmarks to assess your competitiveness.

Business-Specific Goals: Establish specific goals based on your business’s unique needs and growth aspirations.

Regular Reviews: Conduct periodic reviews to evaluate progress toward your targets and adjust strategies as needed.

5.2. Technology and Software

How Financial Software Can Help You Monitor and Optimize Your CCC:

Leverage financial software and technology to streamline CCC management:

Automated CCC Calculations: Use accounting software that can automatically calculate your CCC based on real-time data.

Cash Flow Forecasting Tools: Implement cash flow forecasting tools to predict future cash needs and opportunities accurately.

Data Analytics: Employ data analytics to identify trends and patterns in your CCC, helping you make informed decisions.

Popular Tools and Platforms for SMEs: Consider using popular tools and platforms designed for SMEs:

QuickBooks: QuickBooks offers a range of features to manage finances, including cash flow tracking and forecasting.

Xero: Xero provides cloud-based accounting software that simplifies financial management and cash flow analysis.

Zoho Books: Zoho Books offers accounting and invoicing solutions with cash flow forecasting capabilities.

Excel and Google Sheets: For businesses on a budget, spreadsheet software can be used to create custom CCC tracking templates.

By harnessing technology and software, you can more efficiently monitor and optimize your CCC, ensuring your SME’s financial health.

Chapter 6: Some Case Studies

In this section, I will present a case studies of SMEs that successfully optimized their CCC. These case studies will showcase different industries, challenges, and solutions:

Case Study 1: Retail Business – “Streamlining Inventory Management”

Background:

A small retail business faced challenges with excess inventory and slow sales turnover. This resulted in tied-up capital and cash flow constraints.

Solution:

The business implemented efficient inventory management practices, including ABC analysis, safety stock management, and Just-in-Time (JIT) inventory techniques. They also improved demand forecasting and supplier relationships.

Results:

DIO reduced from 60 days to 35 days.

Cash flow improved as working capital was released.

Capital was reinvested in marketing efforts, leading to increased sales and profitability.

Case Study 2: Manufacturing Company – “Optimizing Receivables and Payables”

Background:

A manufacturing company faced challenges with late customer payments and the need for more favorable supplier terms.

Solution:

They revised credit policies, offering early payment discounts to encourage prompt customer payments. Simultaneously, they negotiated extended payment terms with key suppliers. Cash flow forecasting was also implemented to schedule payments effectively.

Results:

DSO decreased from 45 days to 25 days.

DPO extended from 30 days to 45 days.

Improved cash flow allowed the company to invest in R&D, leading to innovative product development.

Case Study 3: Service-Based SME – “Enhancing Supplier Relationships”

Background:

A service-based SME faced cash flow challenges due to short DPO and inconsistent revenue streams.

Solution:

The business focused on building strong relationships with suppliers, which allowed them to negotiate extended payment terms. They also implemented cash flow forecasting to align payment schedules with revenue collection.

Results:

DPO extended from 15 days to 45 days.

Cash flow became more predictable, reducing financial stress.

The business had the resources to invest in marketing, resulting in increased client acquisition and revenue growth.

These case studies highlight the practical application of CCC optimization strategies in real-world scenarios. They demonstrate that by addressing specific challenges and implementing tailored solutions, SMEs can significantly improve their cash flow and overall financial health.

Chapter 7: Conclusion and Action Plan

In the final section, we’ll summarize the key takeaways from this comprehensive guide and provide you with a step-by-step action plan:

Summary of Key Takeaways:

The Cash Conversion Cycle (CCC) is a critical financial metric for SMEs that measures how efficiently they manage their working capital.

The CCC consists of three components: Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO).

An optimized CCC leads to improved cash flow, efficient working capital utilization, and enhanced profitability.

Strategies to optimize each CCC component include inventory management techniques, credit policies, supplier negotiations, and cash flow forecasting.

Monitoring KPIs and leveraging technology can help SMEs continuously improve their CCC.

Action Plan for CCC Optimization:

Assessment: Calculate your current CCC to establish a baseline. Identify areas that need improvement, such as DIO, DSO, or DPO.

Strategic Planning: Develop a tailored strategy for optimizing your CCC. Consider the specific challenges your business faces and the industry you operate in.

Implementation: Execute your CCC optimization plan, which may involve improving inventory management, credit policies, supplier relationships, or cash flow forecasting.

Monitoring: Regularly track your CCC and related KPIs to evaluate progress. Adjust your strategy as needed based on the results.

Technology Integration: Explore financial software and tools that can automate CCC calculations and streamline cash flow management.

Continuous Improvement: CCC optimization is an ongoing process. Continuously seek ways to refine your strategy and enhance your working capital management.

Review and Adapt: Periodically review your action plan to ensure it remains aligned with your business’s evolving needs and goals.

By following this action plan and utilizing the knowledge and strategies provided in this guide, SMEs can effectively harness the power of the Cash Conversion Cycle to ensure financial stability and prosperity.